[Product Roadmap] How CASHe used proprietary tech and credit writing systems to disburse Rs 2,500 Cr in loans

Written on: tháng 7 06, 2021

Title : [Product Roadmap] How CASHe used proprietary tech and credit writing systems to disburse Rs 2,500 Cr in loans

link : [Product Roadmap] How CASHe used proprietary tech and credit writing systems to disburse Rs 2,500 Cr in loans

[Product Roadmap] How CASHe used proprietary tech and credit writing systems to disburse Rs 2,500 Cr in loans

A report by global wealth management firm Credit Suisse reveals that Indian fintech startups have raised $10 billion in funding in the last decade, with digital lenders raising $2.5 billion.

Alongside, India saw a burgeoning need for credit – especially for certain underserved segments.

Yogi Sadana and Raman BV decided to solve for this problem and in 2016 founded CASHe, a digital lending startup that caters to the financial needs of professionals aged 25 to 35 years.

“We wanted to challenge the status quo of the digital lending business in India, using technology to change the entire delivery system seamlessly. We looked at the prevailing credit business in India and abroad to create a unique business model,” Yogi says.

The founders realised that the idea of credit is invariably linked to a borrower’s credit rating. A borrower will not qualify for a loan if the rating provided by the credit bureau does not pass muster with financial institutions.

The duo also found that most young professionals, especially those new to the workplace and seeking a loan, did not have a prior credit history.

“This is when the big idea struck us. We needed a solution that gave the lending business a fresh perspective. We focused on millennials as we believed they have common traits across the world.

"CASHe was launched with a clear purpose to provide India’s urban working millennials with a path to better financial health, with the aid of technology through their smartphones,” Yogi says.

CashE team

What it does

In a smart digital world, the CASHe app aims to offer quick and easy personal loans through processes that are “transparent and tuned to the times”.

The fintech startup has an automated and robust credit lending system, and the AI-based algorithm - developed in-house - assesses the risk of a borrower based on the user’s social and mobile data footprints.

The model goes beyond traditional credit-risk metrics and assesses the borrower’s “goodness quotient” and the ability to repay. Hence, CASHe lends to young working professionals who are either near-prime or subprime borrowers with or without a prior credit history.

“We operate in a digital world that surpasses that of a high-touch model in terms of scalability. We have used a combination of AI and big data to build an engine that trains, learns, adapts, and predicts human behaviour - otherwise a monumental task.

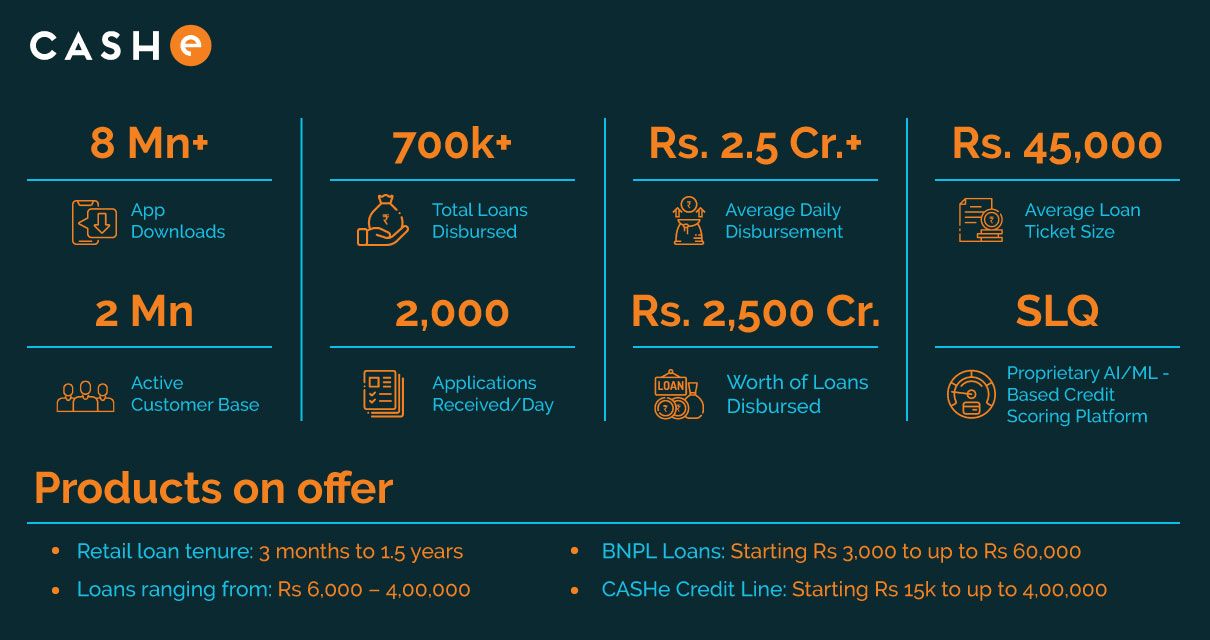

"The cumulative loan disbursement for CASHe stands at Rs 2,500 crore since the launch of operations. Our growth in disbursement percentage-wise is around 30 percent on a month on month, with an overall active customer base of around three lakh,” Yogi says.

Starting small

From ideation to raising funds and having the right set of people to create the tech, it took the CashE team six months to start rolling out its services. They began with 15 and 30-day loan products.

Yogi says the concept of availing hassle-free loans through a smartphone was relatively new in India around five years back.

“We were encouraged with the response and saw a huge increase in the trend of getting a loan through a technology platform like CASHe. Coming up with that unique app idea is often the easiest part.

"Creating and developing our industry-first proprietary tech algorithm with very little or no data was a challenge. The predictive engine was a work in process as it continued to learn from every transaction. Launching upgrades every week to keep the app best-in-class and stay ahead of everyone else in the marketplace helped us to stay ahead of the competition.”

The purpose of an MVP was to gather validated learning from a minimal amount of effort. The build-measure-learn process helped release the product, with the flexibility to bring in changes based on user feedback and plan future updates for better service.

Using data to grow

The gathered data helped the tech team introduce many features on the go, creating a better borrowing experience for users.

“We ran the MVP for around three months with a set of potential customers. The feedback received were encouraging and the learnings ensured further improvements, and we launched the service across India in 2016,” Yogi says.

The aim was to disrupt the Indian lending landscape and ensure true financial inclusion. CashE provides loans to those who otherwise cannot get loans through the traditional credit system. The lack of financial data and credit history makes them suboptimal borrowers for traditional lenders.

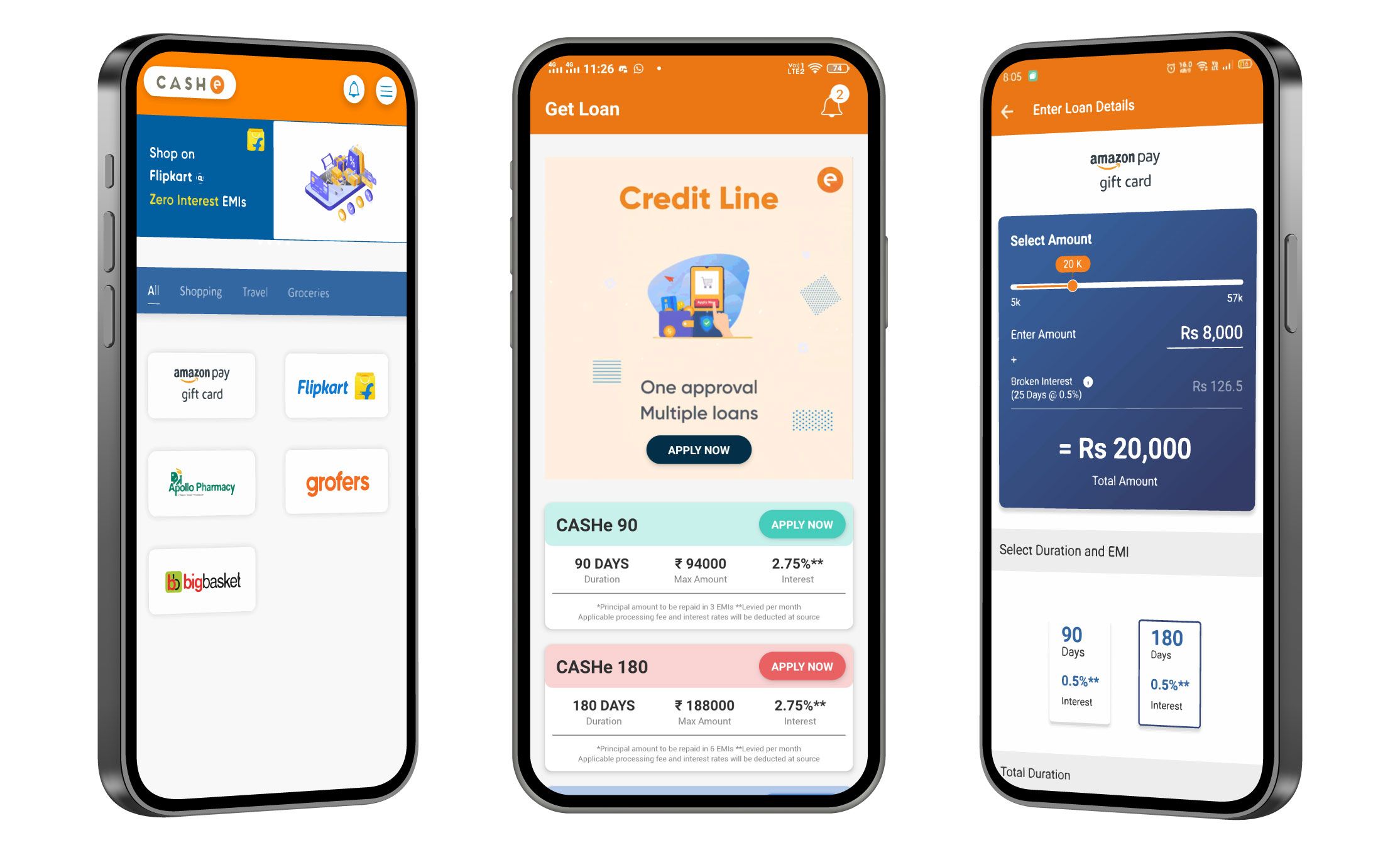

Yogi says the current business model is fully scalable as it enables the team to offer value-added services. CASHe was the first fintech lender to debut on Google Pay, offering short-term loans to Google Pay customers.

Credit line, BNPL, and customer feedback

The team has also launched a credit line facility, which provides customers with funds based on their eligibility. Customers can also utilise part of their funds as a buy now, pay later loan to shop at online shopping sites and return in easy, low-cost EMIs.

With long-term recurring revenue streams associated with all these services, Yogi says CashE is one of the few fintech lenders that turned profitable within two years of starting operations.

“We believe it is important not to be satisfied with just incremental product improvements. We need breakthrough development and innovations in the business models to offer unique solutions,” he adds.

CashE introduced short-term lending for those who faced a month-end financial crunch. “We slowly but regularly expanded our product offerings to reach out to a larger mass of people so they benefit from our technology and services.”

Constant product improvement was facilitated by putting in place a customer feedback loop.

Yogi says this gives them an advantage over the competition, creating a high-quality customer experience and allowing them to offer new services that users want.

“Results from the user feedback loop led us to expand our product offerings. We introduced higher value loan products, decreased the time to apply for a loan, and made the user experience less cumbersome,” Yogi says.

The tech that helped with ‘no-file’ consumers

Low credit penetration, particularly low unsecured credit, is primarily because Indians tend to be 'thin-file' or 'no-file' customers from the point of view of traditional lenders.

The program, SLQ, uses a combination of big data analytics and proprietary AI-based algorithms to evaluate inputs and the user’s digital footprint to measure their credit worthiness.

It measures a borrower’s propensity to repay - based on currently available information - as opposed to traditional credit scoring systems that deliver a score based only on historical financial behaviour.

This means an individual with no financial history can get a loan from CashE if the SLQ engine determines they have a “reasonable propensity to repay”. “This is a unique feature and we have successfully created a large customer base.”

Apart from the seamless, new-age digital lending experience, the team also experimented with marketing tactics, advertising efforts, web design decisions, and other tasks to quickly convert leads and generate sales. Aggressive customer acquisition campaigns were run on social platforms, and they also looked at electronic media such as television and radio.

“We attempted to achieve growth across as many metrics as possible, most often using low-cost marketing to achieve results.

"For instance, we could gain rapid growth through a barrage of paid advertising. Our growth hacking strategies encompassed content marketing, steep waiver on fee as an incentive, social media, and similar tactics. Their chief asset was often in the creativity and we successfully scaled the business by reaching as many uses as we could,” Yogi says.

Challenges along the way

CashE’s AI-based credit scoring platform was built in-house completely.

“We chose our internal crack team of around 15 technology specialists to build the platform from scratch. We later added specialists, including developers and data scientists, to help build and scale the platform,” Yogi says.

However, the team has had its share of challenges, beginning with the fact that technology moves at an incredible speed and keeping up can be challenging. Finding and hiring the right talent for a new product/service category was also tough.

Other challenges included planning components that would be part of the user experience for the best usability standards, figuring out the best security and data protection practices, and ensuring the app technology and business approach complied with government regulations.

The founders invested in cutting-edge technology to build and scale the platform. They developed a roadmap for the future by determining the capabilities the platform would need to remain competitive and innovative. Cloud technology thus become central to their transformation efforts.

Market and the future

In 2020, the Reserve Bank of India (RBI) issued notifications to Non-Banking Finance Corporations (NBFCs) and banks, mandating additional disclosures/compliances and an advisory to borrowers warning them against fraud platforms.

The Digital Lenders Association of India (DLAI) has also issued guidelines, with a regulatory pipeline.

Fintech players like CashE continue to thrive due to compliance with RBI guidelines. It competes with platforms like EarlySalary and PayMe India that follow a similar model.

“We want to be an agile organisation. Our goal is to build a large financial model and to reach every touch point of our customers’ financial lives with products and services that are unique and differentiated.

“Our goal is to increase customer acquisition 5X and double our size in the next six months. We will be part of a vibrant financial ecosystem that will drive new collaborations and build unique business models to increase customer convenience and bring more value to the company,” Yogi says.

Edited by Teja Lele Desai

Link : https://yourstory.com/2021/07/product-roadmap-fintech-startup-cashe-loans-millennials

Author :- Sindhu Kashyaap ( )

July 07, 2021 at 06:00AM

YourStory

That's the article [Product Roadmap] How CASHe used proprietary tech and credit writing systems to disburse Rs 2,500 Cr in loans

You are now reading the article [Product Roadmap] How CASHe used proprietary tech and credit writing systems to disburse Rs 2,500 Cr in loans with link address https://updateboynew.blogspot.com/2021/07/product-roadmap-how-cashe-used.html